In an exclusive snippet from Knight Frank’s Autumn Research Report for Hotel News ME, Ali Manzoor, associate partner, Knight Frank weighs in on the impact of holiday homes opening up in the region on hotels as the lure of paying less becomes an attractive prospect for tourists.

While peer-to-peer markets have been operational in more mature markets for quite some time, they have a less storied history in Dubai. Well-established platforms such as Uber, Zopa, and Craigslist have been replicated in the emirate to some degree (i.e. Careem, Beehive and Dubizzle), however there is still ground to cover in terms of user base and market reach before they can be considered to be fully comparable to their global counterparts.

When Decree Number 41 of 2013 was passed (which outlined the framework under which holiday homes could be operated in Dubai), yet another peer-to-peer market – in the form of short-term rentals – started to gain traction in the emirate. At the time, one key stipulation of the legislation was that it was necessary for home owners to engage a licensed third-party holiday home operator as a management company in exchange for a fee, which typically ranged from 20 to 25% of gross revenues.

While such management companies still exist, these regulations were relaxed in April 2016, with the DTCM allowing individual home owners to apply for holiday home licenses directly without having to commission a third-party. The net effect has been a rapid increase in supply of short term rentals over the past months, as increasing numbers of home owners test the depth of the market.

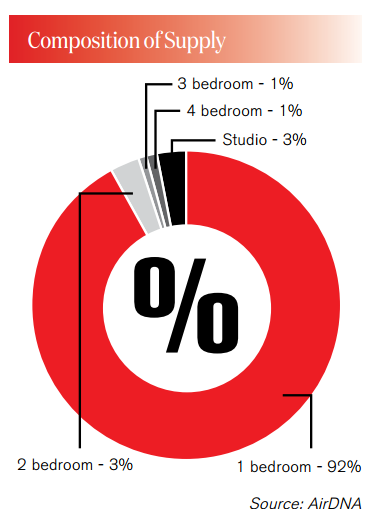

Holiday home supply

While units are typically marketed through multiple platforms such as Dubizzle and booking.com, Airbnb is generally viewed as the market leader for short-term rentals. A look at ‘active listings’ on Airbnb (i.e. listings which have been live in the last thirty days) indicate that there are currently 4,240 units available, of which 24% are private rooms, 6% are shared rooms and the remaining are entire units. Although shared hosting has long since been a hallmark of the Airbnb experience, it technically is not permissible under current legislation and the authorities have actively engaged in putting a stop to this practice.

On a Dubai-wide basis, the unit mix almost exclusively comprises one-bedroom units, accounting for 92% of total supply. Primary interviews amongst operators indicate that such units are in high demand as they are the most versatile, given that they are able to accommodate from one to four individuals if a sofa bed is provided. Two and three bedroom units are comparatively more difficult to rent, not only because they are more expensive, but also because demand is highly seasonal, peaking during public holidays.

Holiday homes are primarily located in The Palm Jumeirah, Dubai Marina, Jumeirah Beach Residences, DIFC and Downtown Dubai – all areas that have high concentrations of hotel supply. Whereas in many other markets, holiday homes are primarily located outside of traditional hotel districts, this is not the case for Dubai, which may prove to be problematic for the emirate’s hospitality sector in the long-run.

Holiday home demand

While areas such as the Palm Jumeirah and Dubai Marina are dominated by short stay visitation, Downtown Dubai and DIFC have a much higher proportion of long stay demand seeking out monthly contracts.

The short stay market is primarily driven by guests from GCC and Europe, within which a significant share of visitors come from Saudi Arabia and the United Kingdom. Short stay demand typically peaks during public holidays and school vacations and Dubai Marina and JBR are typically the most sought after locations.

Guests who utilise holiday homes by the month tend to either be unwilling to commit to traditional annual rental contracts or in some cases are involved in project work that takes them out of the emirate for months at a time.

Key Performance Indicators

When examining the achievable rates of the holiday home sector in relation to the hotel sector, it is clear that the former has outperformed the latter consistently since November 2015. This can partially be explained by the fact that holiday home supply is highly concentrated in high-income areas such as JBR and Downtown Dubai. By contrast, hotel supply is distributed more evenly throughout Dubai, and is inclusive of submarkets such as Deira, in which the achievable rate has historically been low. As more holiday home units come online in secondary and tertiary areas, it is likely that this ADR premium will erode in the long-term.

Impact of holiday homes on the hotel market

Although hotel operators were initially dismissive of the holiday home market when it was at its nascent stages, generally citing that it either catered to a different demand base or was a different product offering, over time this view has been abandoned. Many operators have since acknowledged the impact that platforms such as Airbnb have had on the hospitality sector, and in some markets have even lobbied for protective legislative measures. The most compelling study carried out on this topic was by Zervas, Proserpio and Byers of Boston University, which came to two critical conclusions:

- Not all hotels are affected equally. The impact of the holiday home market was much more severe for (i) lower priced hotels, (ii) leisure-oriented hotels, (iii) hotels with fewer facilities (iv) hotels without international operators in relation to the remaining stock.

- Holiday homes dilute the ability of hotels to yield during periods of peak demand. Whereas hotel room supply is fixed and the incremental cost of developing supply is very high, the holiday home market can scale appropriately to demand with negligible marginal costs for additional supply. For this reason, they restrict the ability of hotels to price aggressively during periods of peak demand and have the highest impact in markets that are heavily seasonal.

From a supply perspective, hotels in Dubai are insulated to some degree from the effects of the holiday home market as supply is largely ‘top heavy’ and internationally branded. Where potential weaknesses lie are in the ability of hotels to price during peak periods, and this will become an issue in submarkets such as the Palm and Dubai Marina – which not only have volatile demand patterns, but also high volumes of holiday home supply.

{kind=link}